Join the Kiwis who are hatching their tomorrow and have invested more than $2 billion with Hatch.

What is FIF tax?

FIF tax is the set of New Zealand tax rules that apply to certain overseas investments, including shares and funds. It exists to make sure offshore investments are taxed fairly alongside NZ investments.

Quick answers: Does FIF tax apply to you?

✅The total cost of your overseas shares, ETFs, or funds exceeded $50,000 NZD at any point during the tax year (1 April–31 March), AND

✅ You are an NZ tax resident

If you answered yes to both questions, then FIF tax rules apply to all those investments for that tax year.

Read more: FIF tax changes in Budget 2026: what NZ Investors need to know

Why FIF tax exists

FIF tax was introduced to ensure overseas investments are taxed fairly and consistently with investments in New Zealand, even when returns come through growth rather than regular income. Without the FIF rules, NZ investors could invest overseas in companies or funds, watch their investments grow over time, and potentially pay very little NZ tax along the way (other than tax on dividends).

Why is FIF tax set at $50,000 NZD?

The $50,000 NZD investment cost threshold was originally introduced so that everyday investors wouldn’t need to deal with complex tax rules on relatively modest overseas portfolios. However, this threshold was set in 2002 and has not been adjusted since.

A lot has changed since then. Inflation has increased, access to overseas investments has become far more accessible, and median weekly income has risen by around 174%. Together, these changes mean it’s now much more common for investors to reach the $50,000 threshold and need to consider FIF tax.

Who does FIF tax apply to?

FIF tax rules apply to investors who have more than $50,000 NZD in Foreign Investment Funds (FIFs) at any point during the tax year between 1 April and 31 March, even for one day. The $50,000 NZD threshold is on the cost price of your overseas investments.

What counts towards the $50,000 FIF threshold?

- US & other international Shares and ETFs

- American Depositary Receipts (ADRs)

- Investments in foreign money market funds (relevant for some Hatch users up until January 2026)

What doesn’t count towards the FIF threshold?

- Australian shares are generally exempt - you can check exemptions using IRD’s tool

- Money held in cash accounts (Uninvested funds on Hatch are held in US bank deposit accounts)

- Gains - FIF is based on cost, not on the market value of your investments

What happens when I cross $50,000 NZD?

If the FIF rules apply to you, you’ll need to work out your total overseas income from your investments to include, along with your individual tax return (IR3) or trust tax return (IR6), when you file your tax return. Generally you can complete your return online via myIR.

- You can check your estimated peak investment cost for the current tax year at any time in the Tax Reports section in Hatch.

- Hatch can do the heavy lifting with our FIF tax calculator when you order a Hatch FIF report after the end of every tax year. See Hatch’s sample FIF report.

- Alternatively, you can work out the income you’ve earned from FIFs on your own using the IRD’s resources and calculator.

- When you start your tax return online, you’ll need to elect to include overseas income.

Common myth: ‘IRD will come knocking on your door!’

Some investors worry that if you cross the FIF threshold, IRD will automatically turn up or contact you straight away. That’s not how it works. There’s no alert that fires the moment your overseas investments pass $50,000 NZD, and IRD isn’t monitoring individual portfolios day by day.

While IRD may not track your $50,000 cost threshold directly, it’s possible for them to receive information about overseas investments through international data‑sharing agreements with around 100 different countries. They can see some offshore holdings, and might follow up if FIF income isn’t reported when they would reasonably expect it to be.

Examples of when you will pay FIF tax

- You make regular investments of $10,000 NZD every year. The FIF rules apply for any tax year where the total cost of your overseas investments was $50,000 NZD or more at any point during the year (the total investment cost, so what you paid, not including gains or losses). In this example, that would occur in the fifth year (assuming you didn’t sell anything).

- For every subsequent year during which your investment cost is above $50,000 NZD at any point the FIF rules will apply.

- If you had $49,000 NZD of shares, bought another $3,000 NZD, then sold $7,000 NZD, the FIF rules would apply. This is because you had shares that cost more than $50,000 NZD ($49,000 + $3,000 = $52,000 NZD) during the tax year, even though only temporarily.

- Following on from the last example, if you sold that $52,000 NZD of shares, FIF rules would only apply the year you owned those shares. In the following year, when you have less than $50,000 NZD invested, the FIF rules would no longer apply.

You can check your estimated peak investment cost for the current tax year at any time in the Tax Reports section in Hatch.

Is FIF based on cost or market value?

This is one of the most common misunderstandings about FIF tax. The $50,000 NZD threshold is not based on the market value of your investments; it’s the cost price (what you paid for them) and doesn’t include any gains or losses.

When wouldn’t the FIF rules apply?

If, for example, you invested $49,000 NZD and it grew in value to $51,000 NZD. The FIF rules don’t apply because your investment cost (that is, what you paid, not including gains or losses) does not exceed $50,000 NZD.

Learn more about your investment cost on Hatch

Does selling before 31 March avoid FIF tax?

No. If your overseas investment cost exceeded $50,000 at any point during the tax year, FIF rules still apply for that entire year — even if you sell before 31 March.

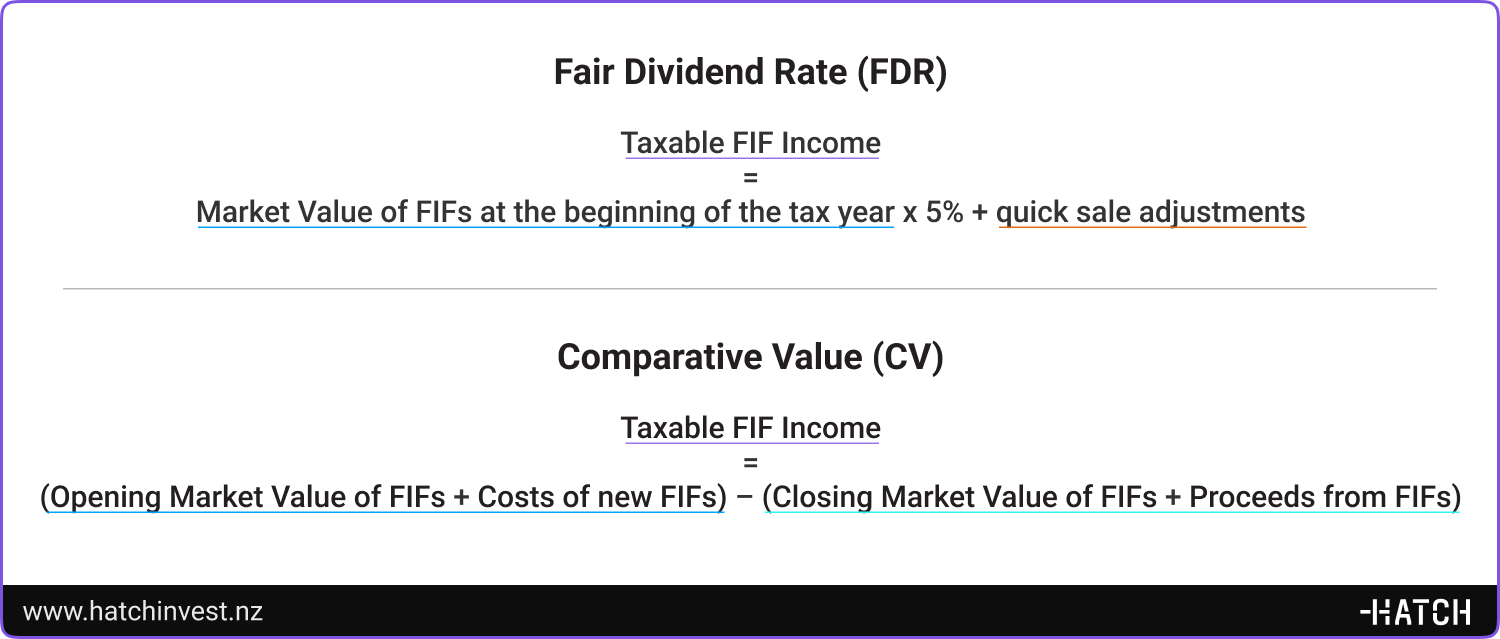

How do I calculate FIF income?

Once you’ve worked out whether the FIF rules apply to your investments, you need to use an approved method to calculate the overseas income which you’ll include in your tax return. FDR (fair dividend rate) and CV (comparative value) are the two most commonly used methods for individuals to calculate their FIF income.

When FDR vs CV is better

Generally an individual can elect to use one method or the other depending on their preference, or whichever gives the lower income. Once you choose your method, you need to use the same one for all FIF investments in any given year.

Hatch provides calculations using both methods in our purchasable FIF report, so you can compare and select your preferred result.

See a sample FIF report from Hatch

What do I need to complete my tax return with FIF income?

Here’s a step-by-step guide to file your tax return in line with the FIF rules and meet your FIF obligations at the end of the tax year.

There are two numbers you need to complete in the ‘overseas investment’ section of your tax return:

- Total claimable overseas tax paid (Step 1)

- Total overseas income earned (Step 2)

Step 1. Find out your total claimable tax paid on overseas income for your Hatch investments

Entering the tax you’ve already paid in the US may result in you receiving a tax credit for some or all of it here in New Zealand. Your annual Tax Reports show the total overseas tax you’ve paid with Hatch, but there’s a little more complexity for FIF taxpayers. We explain here how to work out which investments you can claim a tax credit on.

If you’ve paid tax on overseas investments outside of Hatch, then you’ll also need to include this in your return.

Step 2. Work out your total overseas income for your Hatch investments

To work out your total overseas income, you can order your custom Hatch FIF report. We’ll email it to you as soon as it’s available after the end of each tax year. We can calculate your Hatch FIF income for you, or you can manually calculate your overseas income yourself using the IRD’s resources and calculator.

If you have other overseas investments outside of Hatch, you’ll need to include these in your overseas income calculations too.

Step 3. Fill out your tax return

If you’re paying tax as an individual, you’ll need to complete an IR3 tax return. If you’re a trust, you’ll need to complete an IR6 tax return. It’s easy to do online using myIR.

To complete your individual tax return, you’ll need to use the two numbers you collected earlier:

- Total claimable overseas tax paid (from Step 1)

- Total overseas income (from Step 2)

If you’ve received any other untaxed income outside of Hatch, you'll need to fill out the relevant sections to declare it.

Next steps

If you’re an individual, submit your IR3. There are two ways to go about this:

- Online through myIR. Find the ‘File my individual tax return’ link and complete it online. This will be available at the end of each tax year, after 31 March.

- At the Build your return step select the Overseas income option

- If you’ve received an automatic income tax assessment from IRD, you will need to amend this to include overseas income

- Download and complete an IR3 form manually and send it in using the instructions on the form.

Investing through trusts

For most trusts, FIF applies from the first dollar – regardless of the amount they invest overseas. For this reason, trusts should seek advice early. However, some eligible trusts are only subject to FIF rules if they are above the $50,000 NZD threshold. Additionally, the calculation methods available to a trust can differ from those available to an individual. Check with your accountant or your tax advisor.

Read more: IRD’s Guide to foreign investment funds (FIFs)

Future of FIF – will the FIF rules change?

While the FIF threshold hasn’t changed since 2002, the Government is making some changes to the FIF regime. In March 2026 the Government made some targeted changes to the FIF regime, intended to reduce its impact on new migrants and returning New Zealanders. More changes have been discussed that could make FIF tax compliance less of a burden for individuals, but they’ll need legislation, and would take time to come into effect.

I need more help!

We don’t know your individual tax situation but we are happy to point you in the right direction. If you have any tax questions:

- Dive into our Help Centre articles

- Contact our friendly support team or

- Talk to a tax professional

This article was significantly updated on May 7, 2026 to include new explanations and examples.

We’re not financial advisors and Hatch news is for your information only. However dazzling our writing, none of it is a recommendation to invest in any of the companies or funds mentioned. If you want support before making any investment decisions, consider seeking financial advice from a licensed provider. We’ve done our best to ensure all information is current when we pushed ‘publish’ on this article. And of course, with investing, your money isn’t guaranteed to grow and there’s always a risk you might lose money.

.png)