Join the Kiwis who are hatching their tomorrow and have invested more than $2 billion with Hatch.

You get a notification from your investing app – you’ve received a dividend! One cent? Better than nothing… but what are you supposed to do with that?

Dividends are when companies share profits with their shareholders, usually as cash, and sometimes as additional shares. Over time, and as you invest more, those dividends can start to add up (this writer had one for $5.49 the other day 🤑).

When you receive a cash dividend, you’ve got a few options:

- Leave the cash in your account to invest manually

- Withdraw the cash as income

- Use a dividend reinvestment plan (DRIP/DRP)

Not all investing platforms offer automatic reinvestment – some leave it up to you to decide what to do each time.

What is a DRIP (Dividend Reinvestment Plan)?

A DRIP, also called a DRP, is a dividend reinvestment plan that automatically uses your dividends to buy more shares in the same investment. For some investors it can become a set‑and‑forget way to stay invested.

How does dividend reinvestment work?

For some companies and exchange-traded funds, you receive dividends as cash. In other cases, (such as specific blue-chip NZX-listed stocks) DRIP is activated with the individual company, and you receive shares as a dividend. Dividends are reinvested back into the investment they came from, giving you more shares over time. Not all platforms offer this automatically — in some cases, dividends are paid as cash and you’ll need to reinvest them yourself.

Dividend reinvestment example

Here’s a very basic example using cash dividends.

You own 10 shares at $100 each, with a 5% annual dividend yield

- Over a year, you’d receive $50 in dividends — around $12.50 each quarter.

- If that $12.50 is reinvested, you’ll buy fractional shares, bringing your total to 10.125 shares.

- Next quarter, your dividend is calculated on those extra shares — giving you $12.66 instead of $12.50.

- All of that… for an extra $0.16?

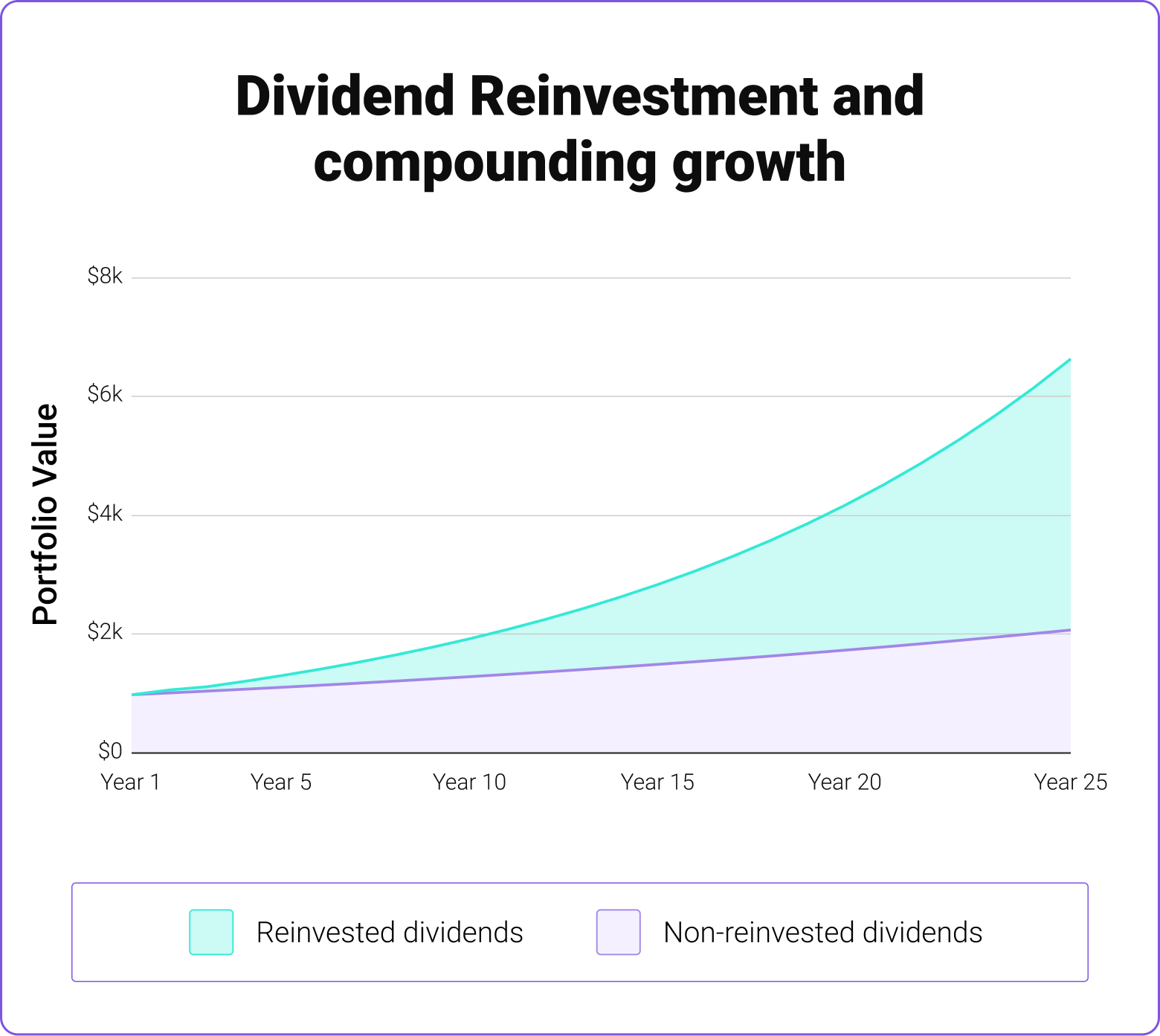

Let’s look at a visual of how compounding growth can work with dividend reinvestment over the long-term.

This is a simplified example that doesn’t account for tax, fees, or market fluctuations. If you’d like to have a go at your own DRIP math, Sharesight has a dividend calculator on their website you can use for free.

Should you reinvest dividends, or take the cash?

Money or the bag? The right answer depends on your investment timeline, your goals, and your circumstances.

Reinvesting dividends could make sense if you:

- Are investing for the long term

- Want to grow your portfolio over time

- Don’t need extra income right now

- Prefer a more hands‑off approach to investing

Taking dividends as cash can make sense if you:

- Want a regular income from your investments

- Are close to (or in) retirement

- Plan to invest the money somewhere else

- Need flexibility for spending, or rebalancing

- Want control over the timing of reinvestment

Are reinvested dividends taxable?

In most cases, yes. Even if your dividends are reinvested, they’re usually still treated as income for tax purposes. How this works depends on your individual situation, so it’s worth checking with an accountant how this could apply to you.

Read more: Tax on shares NZ: when you pay tax (and when you don’t)

Dividend reinvestment vs manual investing — what’s the difference?

The difference mostly comes down to how much you want to automate, versus how much control you want. Some investors prefer the simplicity of DRIPs. Others prefer to make decisions themselves. Depending on the investment platform you use, you can switch between different ways of managing your dividends too.

Reinvesting dividends automatically can also reduce the cost of staying invested, especially over time.

How dividend reinvestment can fit into a long‑term investing strategy

Dividend reinvestment is one way to stay consistent. It aligns with a few core investing ideas:

- Dollar cost averaging – Investing money at regular intervals, with a goal of keeping your average cost price down.

- Compounding growth – The interest your investment earns, as well as the interest your returns earn over time.

- Taking emotions out of investing – Sticking to a long-term investment strategy, and avoiding fear and hype.

Reinvesting dividends won’t guarantee returns — but it can help to keep your money working without needing constant decisions.

How does dividend reinvestment work on Hatch?

With Hatch, you can choose whether your dividends are reinvested or paid as cash, and change that at any time as your strategy evolves.

If you turn on DRP, dividends from all your investments are automatically reinvested back into those same investments. Dividend reinvestment doesn’t incur the usual $3 USD trade fee, so it can be a cost-effective way of reinvesting your funds.

Important things to know about how DRP works on Hatch

- Turn DRP on or off in your account settings.

- This activates DRP for all eligible investments.

- You’ll still see every transaction and dividend notification

- It costs nothing - no $3 USD trade fees.

Help Article: How dividend reinvestment works with your Hatch account

The takeaway

Dividend reinvestment is a simple idea:

- You earn dividends

- You reinvest them

- You gradually build more shares

Over time, those extra shares can start to generate their own dividends — and that’s where compounding growth comes in. It won’t guarantee returns, and it’s not the right approach for everyone. But for long‑term investors, it can be an easy way to stay consistent and keep your money working in the background. Whether you reinvest or take the cash comes down to your goals, your timeframe, and what you need from your investments.

We’re not financial advisors and Hatch news is for your information only. However dazzling our writing, none of it is a recommendation to invest in any of the companies or funds mentioned. If you want support before making any investment decisions, consider seeking financial advice from a licensed provider. We’ve done our best to ensure all information is current when we pushed ‘publish’ on this article. And of course, with investing, your money isn’t guaranteed to grow and there’s always a risk you might lose money.

.png)